Superficially Sentient and the Magnificent Bribe

In a remarkably prescient piece, the social critic Earnest Mumford in ‘Technics and the Nature of Man’, unnervingly anticipates a scenario which could easily pass for today, over half a century ago – long before smart phones or CoPilot. Whilst lengthy, it is worth reproducing some of his sentiments;

The last century, we all realise, has witnessed a radical transformation in the entire human environment, largely as a result of the mathematical and physical sciences upon technology. This shift…..has opened up new realms, such as those of nuclear energy, supersonic transportation, cybernetic intelligence and instantaneous planetary communication.

With these new megatechnics, man will create a new uniform, all-enveloping structure, designed for automatic operation. Instead of functioning actively as a tool-using animal whose proper functions, if this process continues unchanged, will either be fed into a machine, or strictly limited and controlled for the benefit of the depersonalised collective organisation.

Now whilst markets seemed to applaud any company that mentioned AI in last year’s earnings calls, the wider populace is inundated with either utopian visions or doomsday prophecies. At this point, neither is particularly accurate AI has certainly mastered composing certain text, folding proteins or for that matter playing chess and keeping your little ones glued to a screen, but it is yet to harness the technology required to seize a country. Nor are we as yet being literally being ‘fed into a machine’, although whether we are figuratively open to debate.

In a world whose digital litterfall is masses of unstructured data though, AI does of course represent a huge leap forwards in putting order to some of it. This exchange of access to technological systems and benefits thereof, in exchange for compliance, which Mr Mumford described as the ‘magnificent bribe’, could easily be translated to the enhanced productivity brought by ChatGPT, to the exclusion of others (Google, Bing or traditional book bound research).

Economic Fairy Dust

Productivity Growth is the holy grail for market economies. Economic growth reduces to a simple equation – population growth, plus productivity growth and growth in debt. If there are more people, being more productive, then economies have the capacity to bound forwards in a manner that doesn’t leave anybody behind.

It’s difficult to argue that we are not knee deep in another technological revolution, a digital revolution that follows those of the agricultural and industrial ages. In some respects, we can trace its roots back to the 1950’s and the IBM mainframe, which set in motion a technological innovation cycle that is gathering pace.

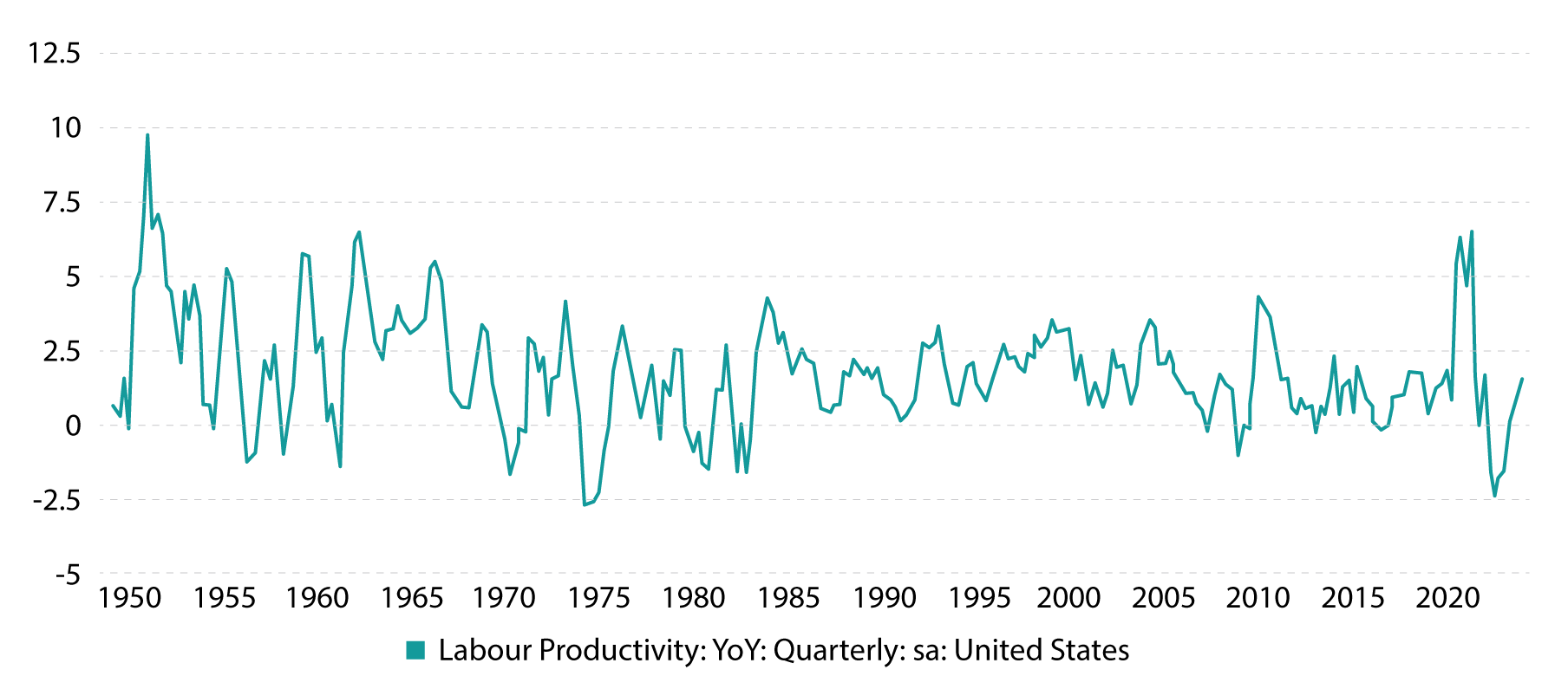

Productivity growth can be measured – and is habitually done, by considering in terms a 5-year trailing average. In that respect, we bottomed during COVID-19 at -2.5%. If we fast forward to Q3 of 2024, we registered a 2.0% trailing average. That’s a significant severalfold increase in less than a decade. Even more intriguing is that when considered through a wider historical lens, 2.0% productivity growth is merely the average clip, meaning we can significantly accelerate from here, where the 50’s saw scores of 5% plus.

Figure 1: US Productivity Growth, QoQ 1950 to 2024

Source: CEICDATA.COM, ARIA

Productivity growth is the fountain of all youth then, it creates economic growth without inflation (it reduces the cost per unit of labour hence dampens (wage) inflation), expands profit margins, creates wealth and reduces debt. It leads to real, sustained GDP growth and material wealth creation that it not simply ‘borrowing’ from the future.

Artificial intelligence means many things to many people, but its essence is increasing the speed with which we process data to draw meaningful conclusions. That drives robotics, autonomous driving, advances in healthcare and improves our ability to recover once economically unviable energy reserves, such as shale oil. All improve productivity and humanity’s lot, not just simply through cheaper energy though, which drives down the cost of production.

The Dark Side of the Moon

It’s beyond the scope of this article, to consider some of the potential concerns arising from the increasing automation of society. Perhaps the most telling example yet, is social media’s cleverly constructed algorithms designed to encourage screen time. Meta and others have discovered that the greed, hate and fear are the most effective tools to encourage user engagement, but this is hardly knocking on the door of the ‘Big Robot Rebellion’ depicted in movies such as “The Terminator”.

However, even before those dystopian concerns materialise in our everyday being, we might also consider whether we have already exaggerated expectations of AI. Large Language Models, or LLM’s, are essentially programs which have been trained with billions of parameters, i.e. fed with data, that when prompted can recount well organised and concise summaries of relevant information. These are drawn from the data sets that the program has been provided with.

Whether it be ChatGPT, Gemini or Claude, impressive results are returned from mundane questions posed to them through a very user-friendly interface. The Google Search for information is under existential threat.

However, the information returned, regardless of the platform used is often similar. In fact, it’s hardly surprising given the training data for many of the AI engines has a large degree of overlap, combined with the similarities in their neural nets and transformers. With that in mind, it does raise the question where an individual AI company’s competitive moat is? Where are the monopoly profits that can be harvested by providing search a service? There’s a parallel that can be drawn between airlines or even browsers, all highly competent in delivering their respective services, but almost indistinguishable and therefore labour under highly competitive market structures and thin profit margins. Moreover, LLM’s, just like airlines, are incredibly capital intensive industries, requiring massive spend to train and maintain those models (aircraft).

So, as it stands, it is currently difficult to anticipate a breakthrough technology which is can dominate the industry and produce monopoly profits, as Amazon ultimately has. The difference with Amazon, is that it clearly had a superior business model to bricks-and-mortar retail, which was discernible from the very beginning. The same cannot be readily said of the AI engines.

Picks and Shovels

Nvidia is one of the stock market darlings of 2024, returning 171% during the course of the calendar year. It more than deserves its moment in the sun with over 70% profit margins as its customers, from Bitcoin miners to data centres and AI engines, scramble to secure its wares.

Moreover, Nvidia, much like the CISCO of the TMT boom, may yet have greater staying power given some of its advantages. For example, CUDA is the software developer platform which AI developers can work with, just like Apple’s IoS or Google’s Android operating platform. With library, tools and enviable, developers can program GPU’s and having been trained on it, creates a stickiness that will not be eroded quickly.

However, for every dollar of revenue Nvidia books, i.e. a chip sold, the customer, be that Microsoft, Meta or other, records a capex item in its own accounts. Given there is a question mark over how this capex and these AI services ultimately are monetised, we must consider the potential for this capex to be written down at some point. Moreover, any industry with those sorts of high margins soon attracts competitors.

Whilst the TMT bubble of the 1990’s witnessed massive capital expenditures, (before topping out in 2000), it wasn’t until 2005 that tech company profits were ultimately realised in earnest. Should investors face a similar 10-year wait, we would expect markets to call time on some very lofty valuations well before that. Alternatively, should AI engines simply mark a stepping stone towards Artificial General Intelligence, (AGI), where AI innovates and learns for itself, rather than simply synthesizing existing data, that would be a step change in humanity, never mind productivity gains.

Currently though, the ‘magnificent bribe’ is underpinned by deteriorating quality of information generated, as the quality of training data sets inevitably recedes at the margin. The low hanging fruit has already been picked and benefits may not outweigh the exclusion of other technologies. Mumford’s commentary is useful in helping to signpost where we’ve come from and where we may be going. Moreover, we would not bet against the larger trend being continued technological advances. However, it may pay to pay heed to those authoritarian warnings of limited alternative technological choices from decades ago…certainly for stock market investors, even if it is premature to be of concern to the wider public just now.

Absolute Return Investment Advisers (ARIA) Limited is authorised and regulated by the Financial Conduct Authority in the UK, with Firm Reference number 527557. A Limited Company registered in England and Wales No: 7091239. ARIA and ARIA Capital Management are trading names of Absolute Return Investment Advisers (ARIA) Limited.

Absolute Return Investment Advisers (ARIA) Limited, is the Dubai branch of the UK parent company and is authorised and regulated by the Securities and Commodities Authority in the United Arab Emirates, under registration number 608032. Contact Address: Office 1004, Park Place Tower, Sheikh Zayed Road, Dubai, United Arab Emirates, PO Box 413670.